Healthcare Interoperability Solutions Market Research Report

Global Healthcare Interoperability Solutions Market Size, Growth & Revenue 2025-2033

Global Healthcare Interoperability Solutions Market is segmented by Application (Healthcare, Biotech, Pharmaceuticals, Government, Research), Type (Health Information Exchange (HIE)_Electronic Health Records (EHR)_Patient Data Integration_Interoperable Software_Health Cloud Solutions), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Industry Overview

Global Healthcare Interoperability Solutions Market Size, Forecast, Segment Analysis, By Type Health Information Exchange (HIE), Electronic Health Records (EHR), Patient Data Integration, Interoperable Software, Health Cloud Solutions By Application Healthcare, Biotech, Pharmaceuticals, Government, Research, By Region (2025 to 2033)

Healthcare interoperability solutions enable seamless data exchange between various health IT systems, allowing for comprehensive patient care. These solutions improve communication, reduce errors, and ensure that healthcare providers have real-time access to complete patient data, enhancing the quality and efficiency of care.

The research study Healthcare Interoperability Solutions Market provides readers with details on strategic planning and tactical business decisions that influence and stabilize growth prognosis in Healthcare Interoperability Solutions Market. A few disruptive trends, however, will have opposing and strong influences on the development of the Global Biometric Lockers market and the distribution across players. To provide further guidance on why specific trends in Healthcare Interoperability Solutions market would have a high impact and precisely why these trends can be factored into the market trajectory and the strategic planning of industry players.

Market Dynamics Highlighted

Market Driver

The Healthcare Interoperability Solutions Market is experiencing significant growth due to various factors.

- • Rising demand for seamless healthcare data exchange

- • Increasing use of cloud-based health solutions

- • Focus on patient data security

- • Growing emphasis on patient-centered care

- • Expansion of telemedicine services

Market Trend

The Healthcare Interoperability Solutions market is growing rapidly due to various factors.

- • Growth in cloud-based healthcare solutions

- • Increasing focus on EHR interoperability

- • Rising adoption of telemedicine

- • Expansion of digital health platforms

- • Greater emphasis on patient data integration

Opportunity

The Healthcare Interoperability Solutions has several opportunities, particularly in developing countries where industrialization is growing.

Challenge

The market for fluid power systems faces several obstacles despite its promising growth possibilities.

Healthcare Interoperability SolutionsMarket Segment Highlighted

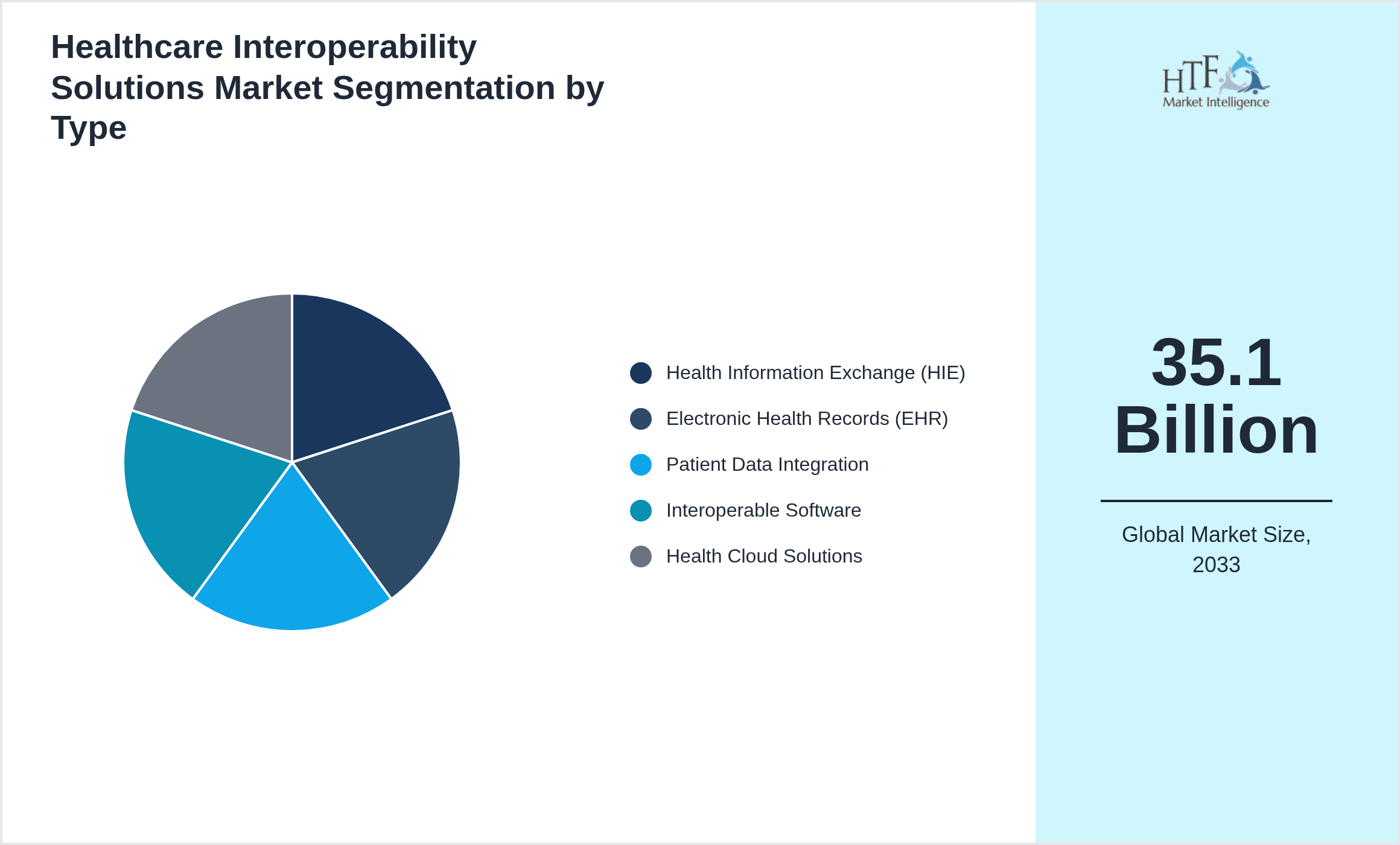

Segmentation by Type

- • Health Information Exchange (HIE)

- • Electronic Health Records (EHR)

- • Patient Data Integration

- • Interoperable Software

- • Health Cloud Solutions

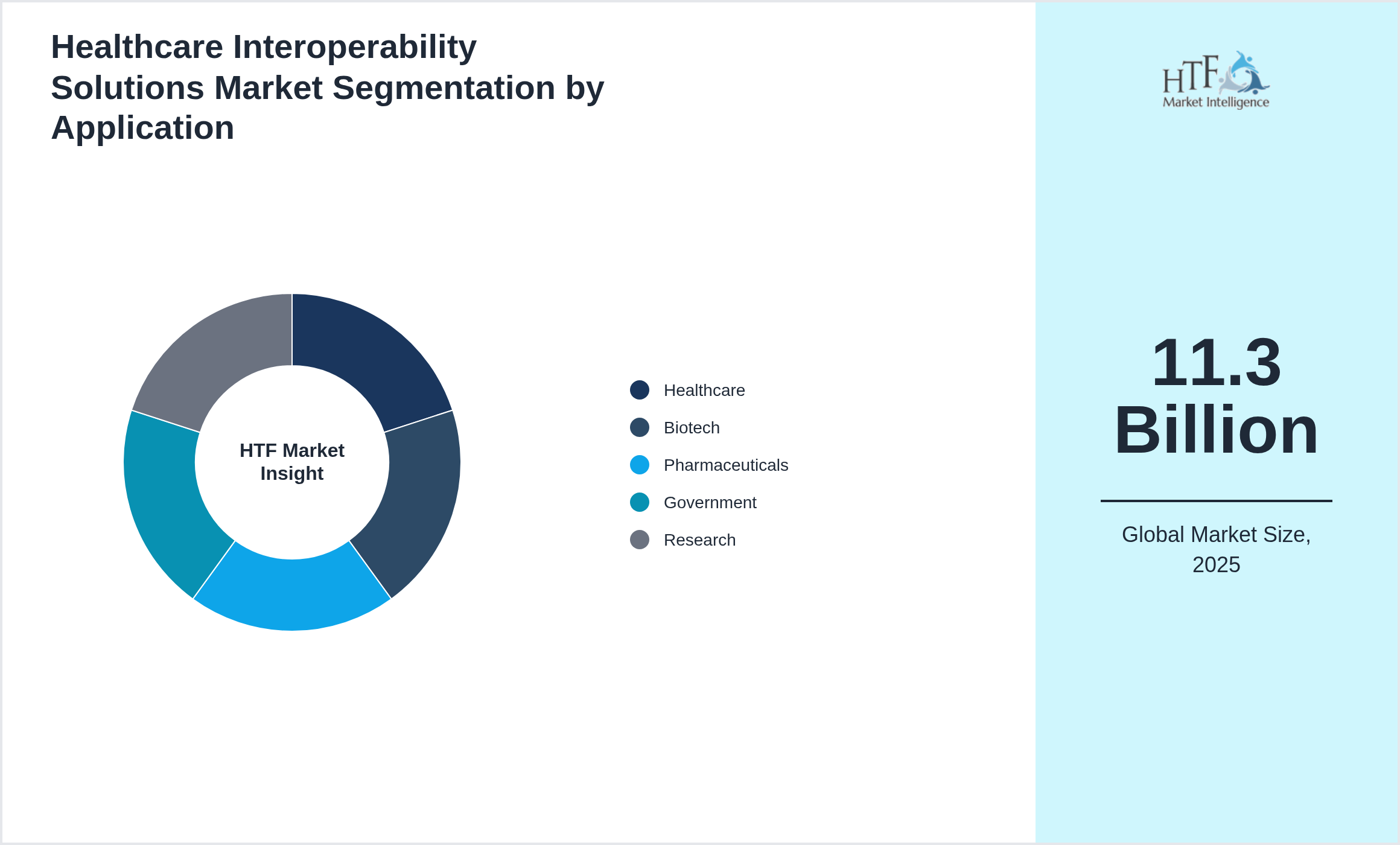

Segmentation by Application

- • Healthcare

- • Biotech

- • Pharmaceuticals

- • Government

- • Research

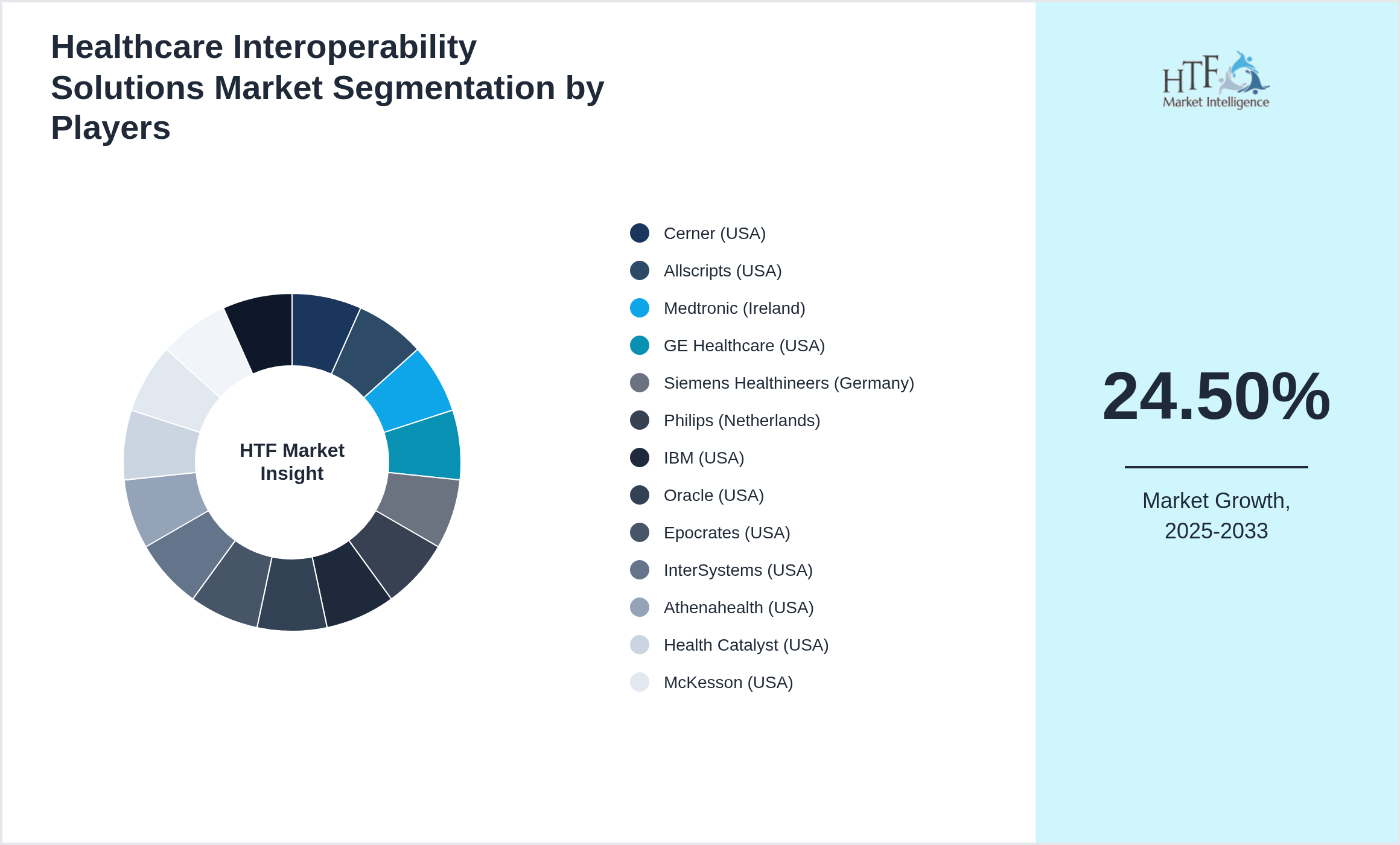

Key Players

Several key players in the Healthcare Interoperability Solutions market is strategically focusing on expanding their operations in developing regions to capture a larger market share, particularly as the year-on-year growth rate for the market stands at 19.20%. The companies featured in this profile were selected based on insights from primary experts, evaluating their market penetration, product offerings, and geographical reach. By targeting emerging markets, these companies aim to leverage new opportunities, enhance their competitive advantage, and drive revenue growth. This approach not only aligns with their overall business objectives but also positions them to respond effectively to the evolving demands of consumers in these regions.

- • Cerner (USA)

- • Allscripts (USA)

- • Medtronic (Ireland)

- • GE Healthcare (USA)

- • Siemens Healthineers (Germany)

- • Philips (Netherlands)

- • IBM (USA)

- • Oracle (USA)

- • Epocrates (USA)

- • InterSystems (USA)

- • Athenahealth (USA)

- • Health Catalyst (USA)

- • McKesson (USA)

- • TietoEVRY (Finland)

- • Optum (USA)

For the complete companies list, please ask for sample pages.

Market Entropy

Merger & Acquisition

Patent Analysis

Investment and Funding Scenario

Market Estimation Process

Key Highlights

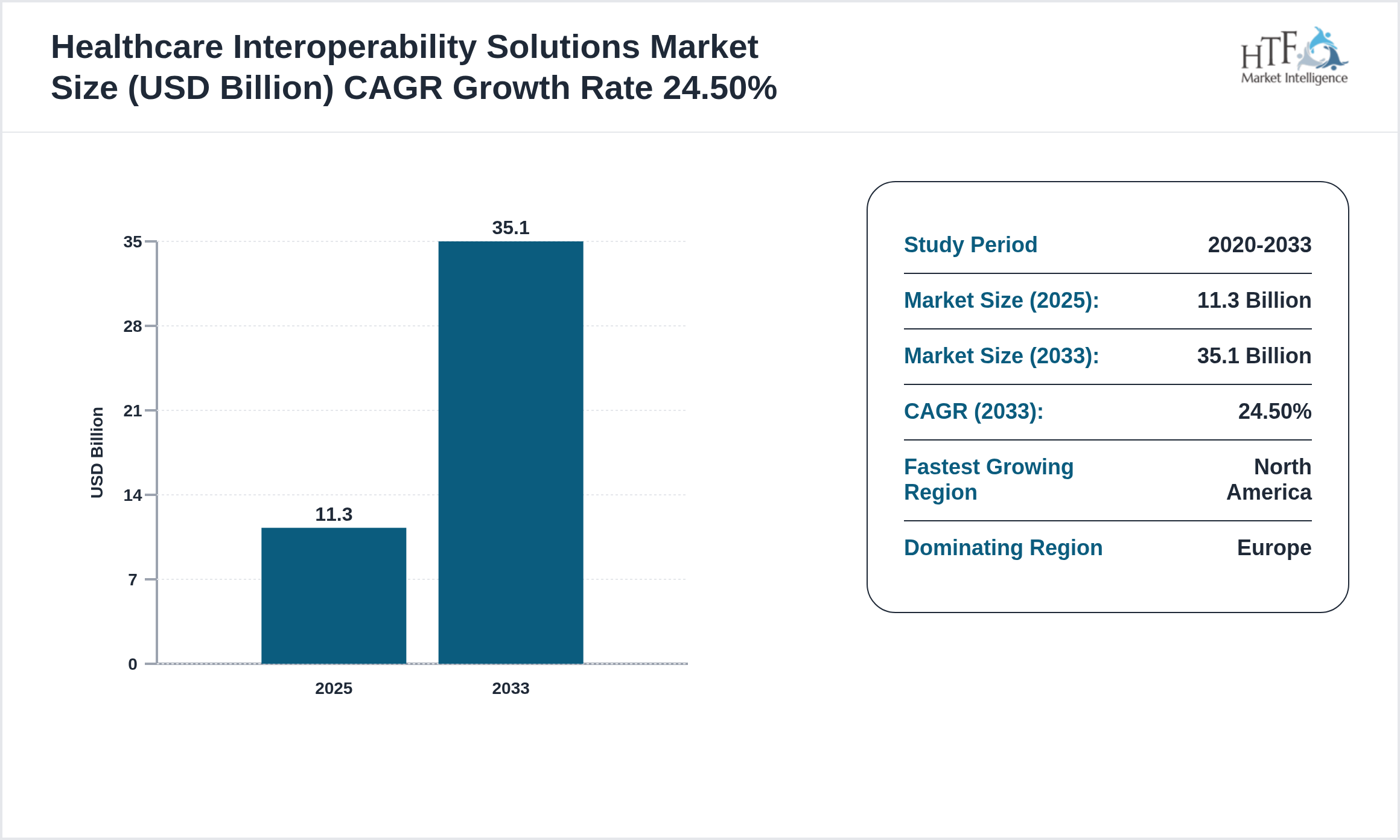

• The Healthcare Interoperability Solutions is growing at a CAGR of 24.50% during the forecasted period of 2025 to 2033

• Year on Year growth for the market is 19.20%

• North America dominated the market share of 11.3 Billion in 2025

• Based on type, the market is bifurcated into Health Information Exchange (HIE), Electronic Health Records (EHR), Patient Data Integration, Interoperable Software, Health Cloud Solutions segment, which dominated the market share during the forecasted period

• Based on application, the market is segmented into Application Healthcare, Biotech, Pharmaceuticals, Government, Research is the fastest-growing segment

• Global Import Export in terms of K Tons, K Units, and Metric Tons will be provided if Applicable based on industry best practice

Our Data Collection Process Based on Best Practice

Problem Definition: Clarify research objectives and client needs & identify key questions and market scope.

Data Collection:

Primary Research: Conduct interviews, surveys, and focus groups.

Secondary Research: Analyzed industry reports, market publications, and financial records.

Data Analysis:

Quantitative Analysis: Use statistical tools to identify trends and quantify market size.

Qualitative Analysis: Interpret non-numerical data to understand market drivers and consumer behavior.

Market Segmentation:

Divide the market into distinct segments based on shared characteristics.

Validation and Triangulation:

Cross-verify findings from multiple sources to ensure accuracy and reliability.

Reporting and Recommendations:

Present insights and strategic recommendations in a tailored, actionable report.

Continuous Feedback Loop:

Engage with clients to refine research and ensure alignment with their goals.

Regional Insight

The Healthcare Interoperability Solutions varies widely by region, reflecting diverse economic conditions and consumer preferences. In North America, the focus is on convenience and premium products, driven by high disposable incomes and a strong e-commerce sector. Europe’s market is fragmented, with Western countries emphasizing luxury and organic goods, while Eastern Europe sees rapid growth. Asia-Pacific is a fast-growing region with high demand for high-tech and affordable products, driven by urbanization and rising middle-class incomes. Latin America prioritizes affordability amidst economic fluctuations, with Brazil and Mexico leading in market growth. In the Middle East and Africa, market trends are influenced by cultural preferences, with luxury goods prominent in the Gulf States and gradual growth in sub-Saharan Africa. Global trends like sustainability and digital transformation are impacting all regions.

The Europe dominant region currently dominates the market share, fueled by increasing consumption, population growth, and sustained economic progress which collectively enhance market demand. Conversely, the North America is growing rapidly, driven by significant infrastructure investments, industrial expansion, and rising consumer demand.

The Top-Down and Bottom-Up Approaches

The top-down approach begins with a broad theory or hypothesis and breaks it down into specific components for testing. This structured, deductive process involves developing a theory, creating hypotheses, collecting and analyzing data, and drawing conclusions. It is particularly useful when there is substantial theoretical knowledge, but it can be rigid and may overlook new phenomena.

Conversely, the bottom-up approach starts with specific data or observations, from which broader generalizations and theories are developed. This inductive process involves collecting detailed data, analyzing it for patterns, developing hypotheses, formulating theories, and validating them with additional data. While this approach is flexible and encourages the discovery of new phenomena, it can be time-consuming and less structured.

Regulatory Framework

The healthcare sector is overseen by various regulatory bodies that ensure the safety, quality, and efficacy of health services and products. In the United States, the U.S. Department of Health and Human Services (HHS) plays a crucial role in protecting public health and providing essential human services. Within HHS, the Food and Drug Administration (FDA) regulates food, drugs, and medical devices, ensuring they meet safety and efficacy standards. The Centers for Disease Control and Prevention (CDC) focus on disease control and prevention, conducting research, and providing health information to protect public health.

In the United Kingdom, the General Medical Council (GMC) regulates doctors, ensuring they adhere to professional standards. Other important bodies include the General Pharmaceutical Council (GPhC), which oversees pharmacists, and the Nursing and Midwifery Council (NMC), which regulates nurses and midwives. These organizations work to maintain high standards of care and protect patients.

Internationally, the European Medicines Agency (EMA) regulates medicines within the European Union, while the World Health Organization (WHO) provides global leadership on public health issues. Each of these regulatory bodies plays a vital role in ensuring that health care systems operate effectively and safely, ultimately safeguarding public health across different regions.

Report Infographics

| Report Features | Details |

| Base Year | 2025 |

| Based Year Market Size (2025) | 11.3 Billion |

| Historical Period | 2020 to 2025 |

| CAGR (2025 to 2033) | 24.50% |

| Forecast Period | 2025 to 2033 |

| Forecasted Period Market Size ( 2033) | 35.1 Billion |

| Scope of the Report | Health Information Exchange (HIE), Electronic Health Records (EHR), Patient Data Integration, Interoperable Software, Health Cloud Solutions, Healthcare, Biotech, Pharmaceuticals, Government, Research |

| Regions Covered | |

| Companies Covered | Cerner (USA), Allscripts (USA), Medtronic (Ireland), GE Healthcare (USA), Siemens Healthineers (Germany), Philips (Netherlands), IBM (USA), Oracle (USA), Epocrates (USA), InterSystems (USA), Athenahealth (USA), Health Catalyst (USA), McKesson (USA), TietoEVRY (Finland), Optum (USA) |

| Customization Scope | 15% Free Customization |

| Delivery Format | PDF and Excel through Email |

Healthcare Interoperability Solutions - Table of Contents

Chapter 1: Market Preface

Chapter 2: Strategic Overview

Chapter 3: Global Healthcare Interoperability Solutions Market Business Environment & Changing Dynamics

Chapter 4: Global Healthcare Interoperability Solutions Industry Factors Assessment

Chapter 5: Healthcare Interoperability Solutions : Competition Benchmarking & Performance Evaluation

Chapter 6: Global Healthcare Interoperability Solutions Market: Company Profiles

Chapter 7: Global Healthcare Interoperability Solutions by Type & Application (2020-2033)

Chapter 8: North America Healthcare Interoperability Solutions Market Breakdown by Country, Type & Application

Chapter 9: Europe Healthcare Interoperability Solutions Market Breakdown by Country, Type & Application

Chapter 10: Asia Pacific Healthcare Interoperability Solutions Market Breakdown by Country, Type & Application

Chapter 11: Latin America Healthcare Interoperability Solutions Market Breakdown by Country, Type & Application

Chapter 12: Middle East & Africa Healthcare Interoperability Solutions Market Breakdown by Country, Type & Application

Chapter 13: Research Finding and Conclusion

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.