Carrier Aggregation Market Research Report

Carrier Aggregation Market - Global Size & Outlook 2020-2033

Global Carrier Aggregation Market is segmented by Application (Mobile Networks, Telecom Operators, Wireless Services, IoT, Consumer Electronics), Type (LTE-A Carrier Aggregation, 5G Carrier Aggregation, Multi-band Aggregation, Sub-6 GHz Aggregation, mmWave Aggregation), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

INDUSTRY OVERVIEW

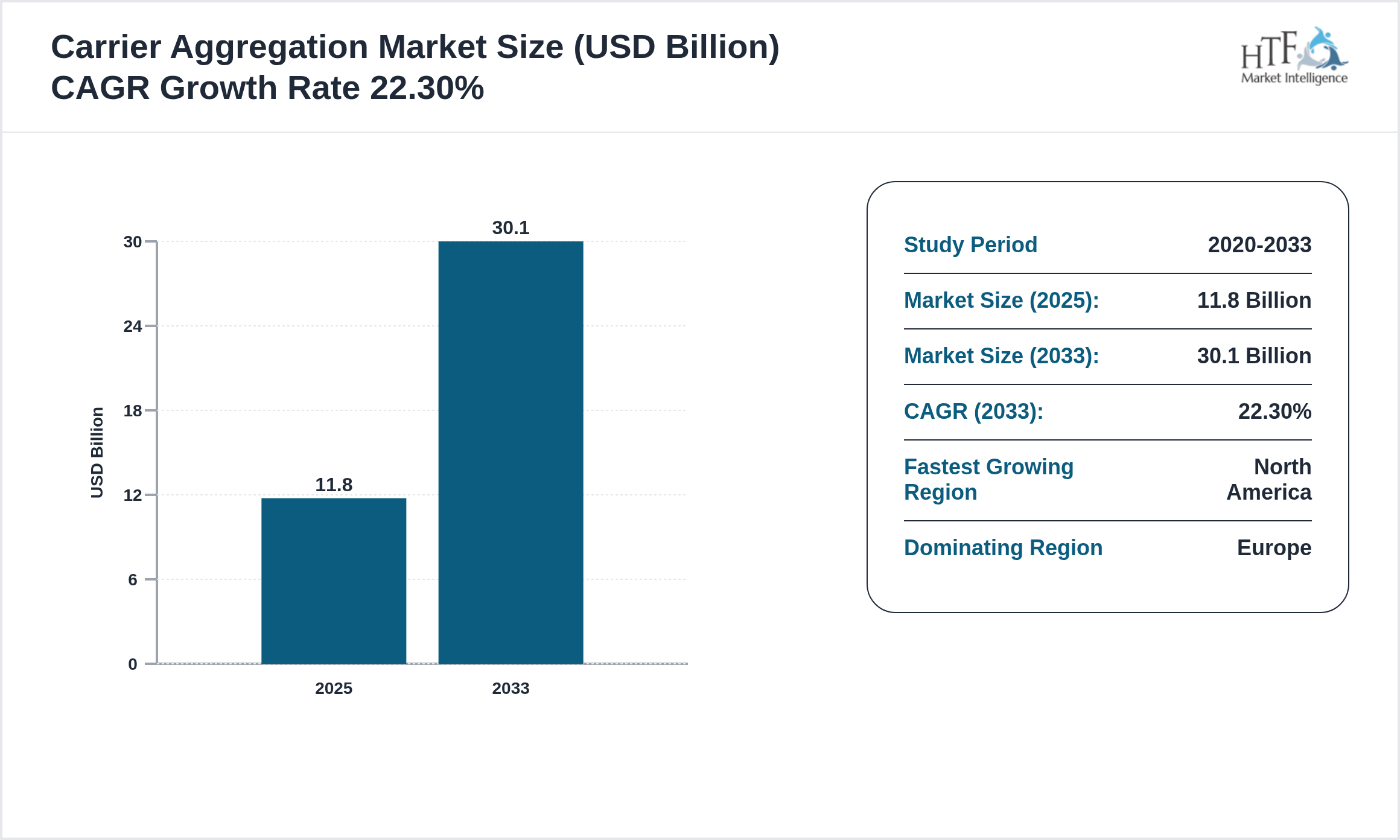

The Carrier Aggregation market is experiencing robust growth, projected to achieve a compound annual growth rate CAGR of 22.30% during the forecast period. Valued at 11.8 Billion, the market is expected to reach 30.1 Billion by 2033, with a year-on-year growth rate of 17.60%. This upward trajectory is driven by factors such as evolving consumer preferences, technological advancements, and increased investment in innovation, positioning the market for significant expansion in the coming years. Companies should strategically focus on enhancing their offerings and exploring new market opportunities to capitalize on this growth potential.

Carrier aggregation enables telecom providers to combine different frequency bands to enhance data speeds and network performance. This technology is crucial for meeting the growing demand for high-speed internet, particularly in 5G networks, by enabling more efficient use of available spectrum.

Regulatory Landscape

- • Regulations focus on spectrum allocation and network management to ensure efficient use of carrier aggregation technologies and to prevent interference between frequencies.

Regulatory Framework

The Information and Communications Technology (ICT) industry is primarily regulated by the Federal Communications Commission (FCC) in the United States, along with other national and international regulatory bodies. The FCC oversees the allocation of spectrum, ensures compliance with telecommunications laws, and fosters fair competition within the sector. It also establishes guidelines for data privacy, cybersecurity, and service accessibility, which are crucial for maintaining industry standards and protecting consumer interests.

Globally, various regulatory agencies, such as the European Telecommunications Standards Institute (ETSI) and the International Telecommunication Union (ITU), play significant roles in standardizing practices and facilitating international cooperation. These bodies work together to create a cohesive regulatory framework that addresses emerging technologies, cross-border data flow, and infrastructure development. Their regulations aim to ensure the ICT industry's growth is both innovative and compliant with global standards, promoting a secure and competitive market environment.

Key Highlights

• The Carrier Aggregation is growing at a CAGR of 22.30% during the forecasted period of 2020 to 2033

• Year on Year growth for the market is 17.60%

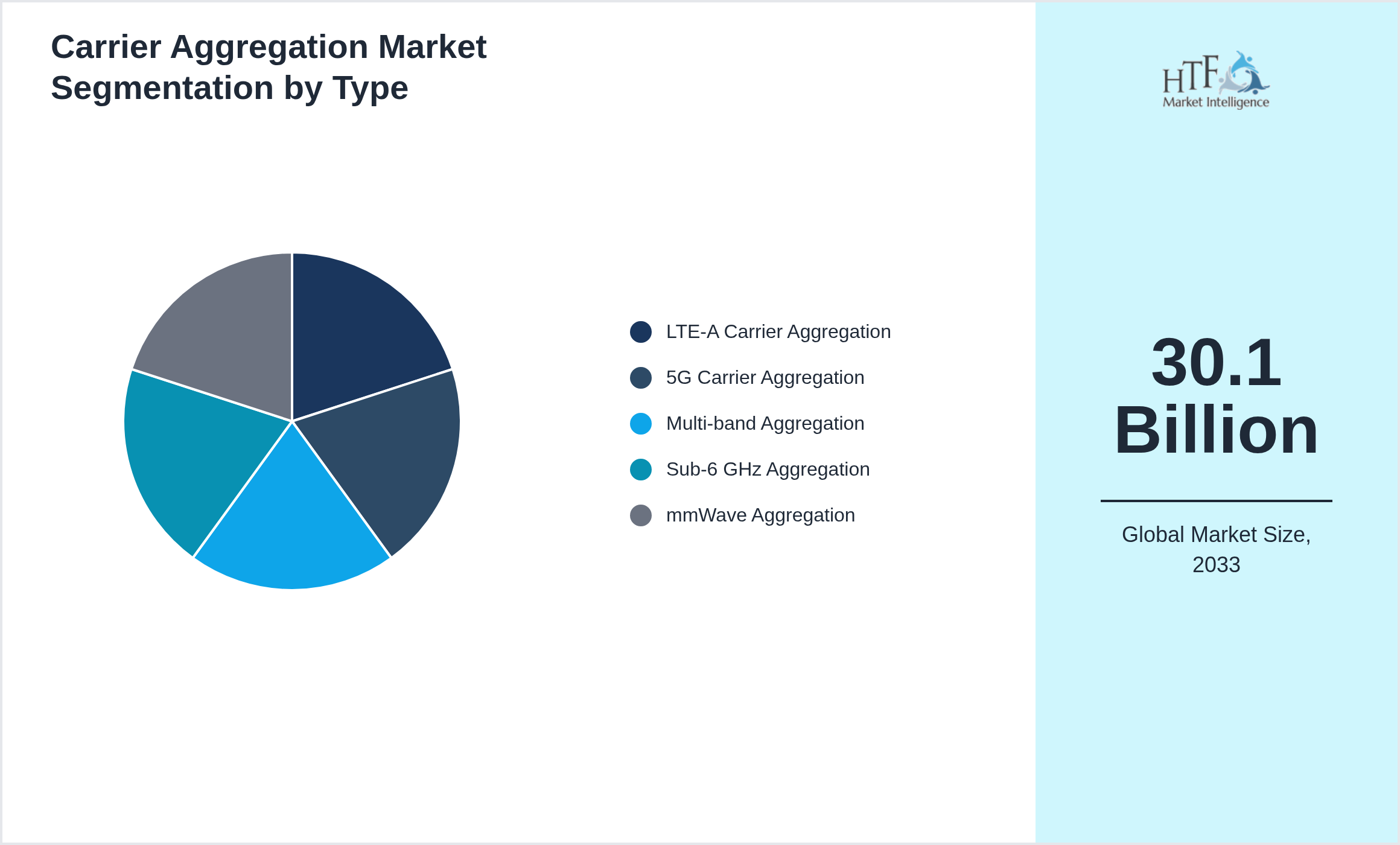

• Based on type, the market is bifurcated into LTE-A Carrier Aggregation, 5G Carrier Aggregation, Multi-band Aggregation, Sub-6 GHz Aggregation, mmWave Aggregation

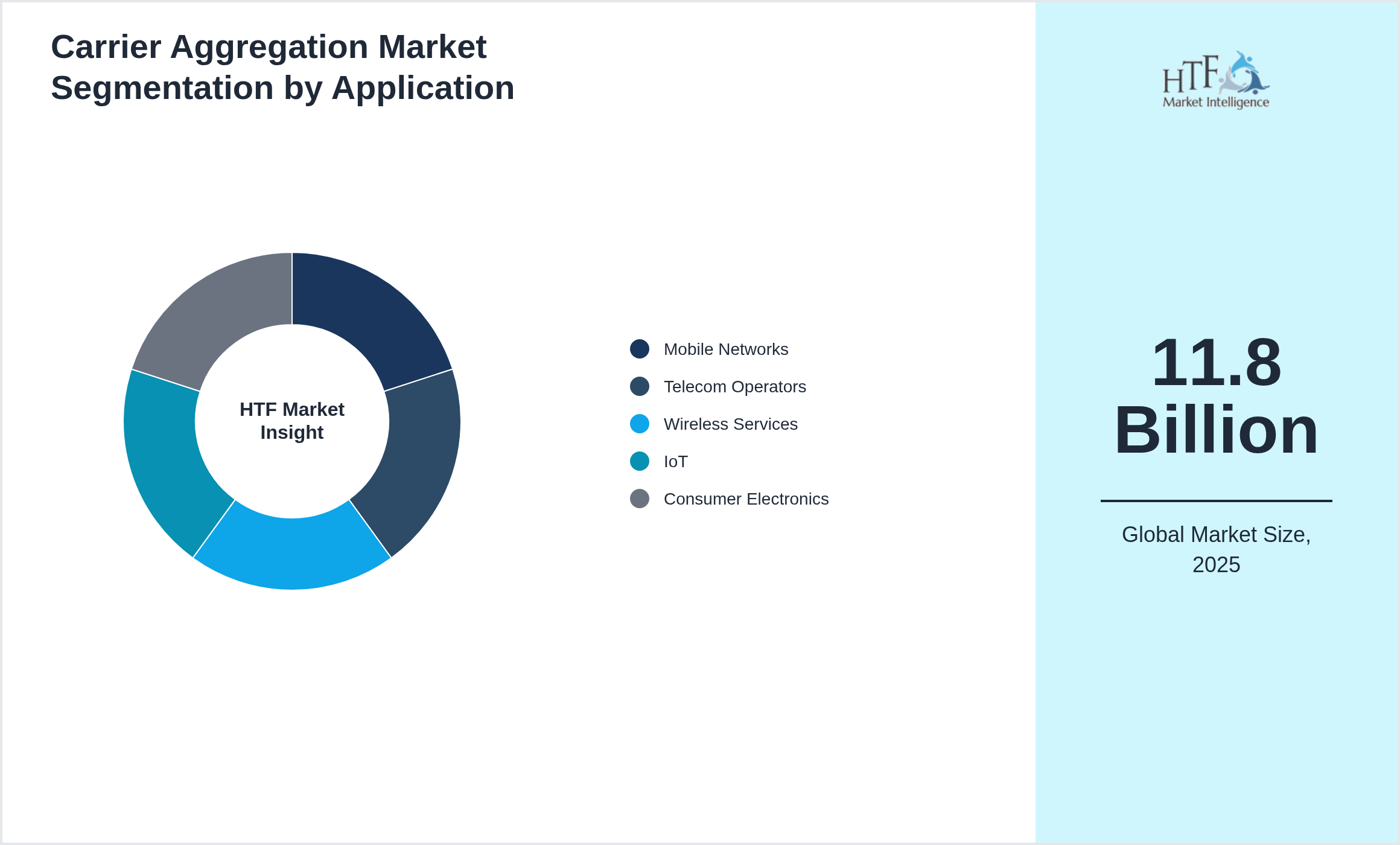

• Based on application, the market is segmented into Mobile Networks, Telecom Operators, Wireless Services, IoT, Consumer Electronics

• Global Import Export in terms of K Tons, K Units, and Metric Tons will be provided if Applicable based on industry best practice

Market Segmentation Analysis

Segmentation by Type

- • LTE-A Carrier Aggregation

- • 5G Carrier Aggregation

- • Multi-band Aggregation

- • Sub-6 GHz Aggregation

- • mmWave Aggregation

Segmentation by Application

- • Mobile Networks

- • Telecom Operators

- • Wireless Services

- • IoT

- • Consumer Electronics

Key Players

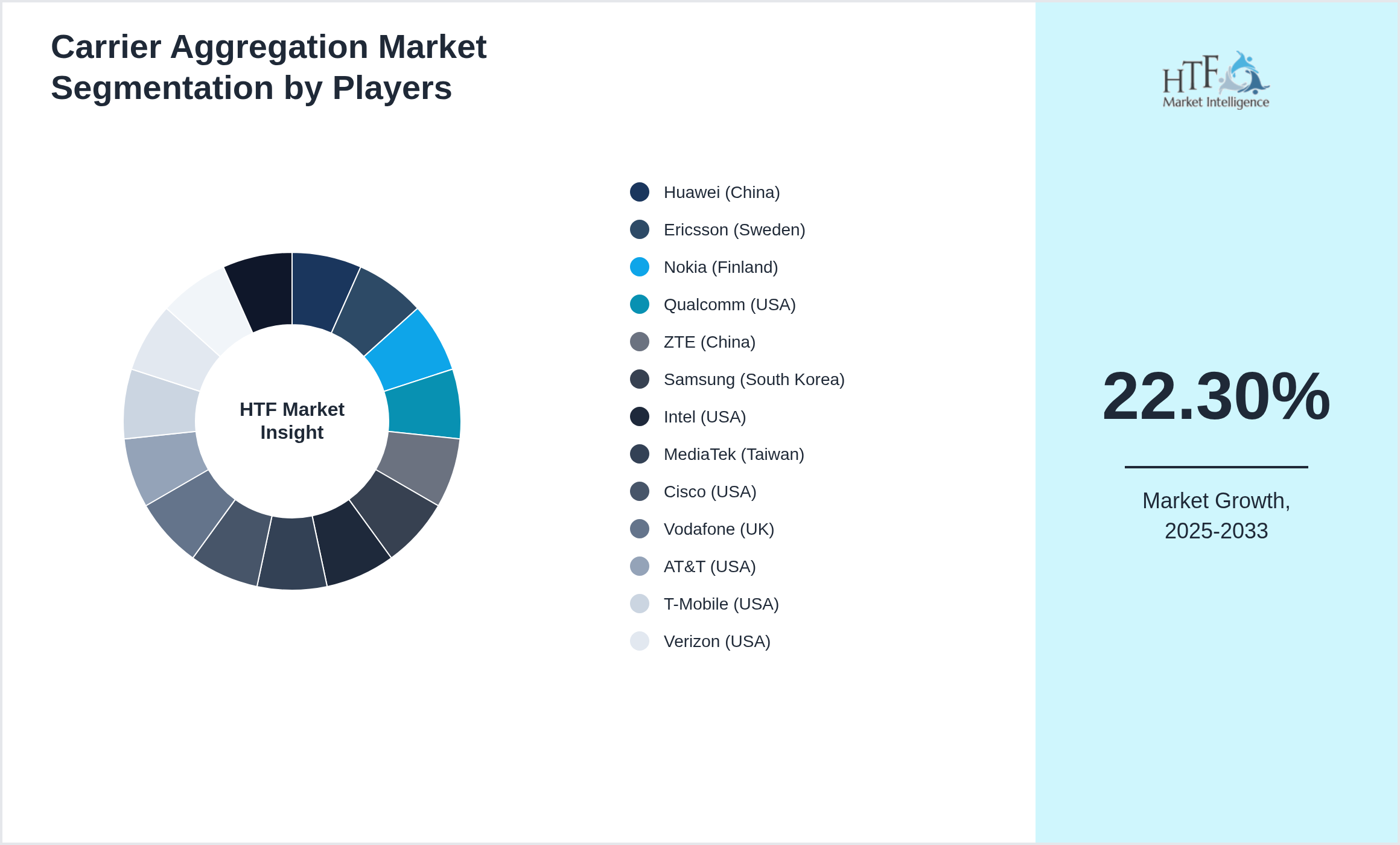

Several key players in the Carrier Aggregation market are strategically focusing on expanding their operations in developing regions to capture a larger market share, particularly as the year-on-year growth rate for the market stands at 17.60%. The companies featured in this profile were selected based on insights from primary experts, evaluating their market penetration, product offerings, and geographical reach. By targeting emerging markets, these companies aim to leverage new opportunities, enhance their competitive advantage, and drive revenue growth. This approach not only aligns with their overall business objectives but also positions them to respond effectively to the evolving demands of consumers in these regions.

- • Huawei (China)

- • Ericsson (Sweden)

- • Nokia (Finland)

- • Qualcomm (USA)

- • ZTE (China)

- • Samsung (South Korea)

- • Intel (USA)

- • MediaTek (Taiwan)

- • Cisco (USA)

- • Vodafone (UK)

- • AT&T (USA)

- • T-Mobile (USA)

- • Verizon (USA)

- • LG Uplus (South Korea)

- • China Mobile (China)

Research Methodology

At HTF Market Intelligence, we pride ourselves on delivering comprehensive market research that combines both secondary and primary methodologies. Our secondary research involves rigorous analysis of existing data sources, such as industry reports, market databases, and competitive landscapes, to provide a robust foundation of market knowledge. This is complemented by our primary research services, where we gather firsthand data through surveys, interviews, and focus groups tailored specifically to your business needs. By integrating these approaches, we offer a thorough understanding of market trends, consumer behavior, and competitive dynamics, enabling you to make well-informed strategic decisions. We would welcome the opportunity to discuss how our research expertise can support your business objectives.

Market Dynamics

Market dynamics refer to the forces that influence the supply and demand of products and services within a market. These forces include factors such as consumer preferences, technological advancements, regulatory changes, economic conditions, and competitive actions. Understanding market dynamics is crucial for businesses as it helps them anticipate changes, identify opportunities, and mitigate risks.

By analyzing market dynamics, companies can better understand market trends, predict potential shifts, and develop strategic responses. This analysis enables businesses to align their product offerings, pricing strategies, and marketing efforts with evolving market conditions, ultimately leading to more informed decision-making and a stronger competitive position in the marketplace.

Market Driver

- • Growing demand for higher data speeds

- • Increasing adoption of 5G

- • Rising demand for mobile broadband

- • Focus on improving network performance

- • Expansion of mobile video consumption

Market Trend

- • Growth in multi-band aggregation for faster speeds

- • Expansion of 5G carrier aggregation

- • Rise in demand for seamless mobile connectivity

- • Increasing use of mmWave for enhanced speeds

- • Focus on improving network capacity

- • Regulatory challenges

- • Spectrum availability issues

- • Integration with legacy networks

- • High cost of deployment

- • Complexity in network management

Challenge

- • Opportunities in 5G network expansion

- • Growth in IoT connectivity

- • Rise in demand for high-speed mobile networks

- • Increased adoption of multi-band aggregation

- • Expansion of seamless mobile experiences

Regional Analysis

- • Carrier aggregation is critical in enabling faster mobile internet speeds and is growing in demand across North America

- • June 2024 – Qualcomm and Ericsson introduced carrier aggregation technologies for 5G networks

- • June

- • Regulations focus on spectrum allocation and network management to ensure efficient use of carrier aggregation technologies and to prevent interference between frequencies.

- • Patents in carrier aggregation focus on technologies that improve data throughput

- • Investment in carrier aggregation technologies is accelerating

Regional Outlook

The Europe Region holds the largest market share in 2025 and is expected to grow at a good CAGR. The North America Region is the fastest-growing region due to increasing development and disposable income.

North America remains a leader, driven by innovation hubs like Silicon Valley and a strong demand for advanced technologies such as AI and cloud computing. Europe is characterized by robust regulatory frameworks and significant investments in digital transformation across sectors. Asia-Pacific is experiencing rapid growth, led by major markets like China and India, where increasing digital adoption and governmental initiatives are propelling ICT advancements.

The Middle East and Africa are witnessing steady expansion, driven by infrastructure development and growing internet penetration. Latin America and South America present emerging opportunities, with rising investments in digital infrastructure, though challenges like economic instability can impact growth. These regional differences highlight the need for tailored strategies in the global ICT market.

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

|

Report Features |

Details |

|

Base Year |

2025 |

|

Based Year Market Size (2025) |

11.8 Billion |

|

Historical Period Market Size (2020) |

USD Million ZZ |

|

CAGR (2025 to 2033) |

22.30% |

|

Forecast Period |

2025 to 2033 |

|

Forecasted Period Market Size (2033) |

30.1 Billion |

|

Scope of the Report |

LTE-A Carrier Aggregation, 5G Carrier Aggregation, Multi-band Aggregation, Sub-6 GHz Aggregation, mmWave Aggregation, Mobile Networks, Telecom Operators, Wireless Services, IoT, Consumer Electronics |

|

Regions Covered |

North America, Europe, Asia Pacific, South America, and MEA |

|

Year on Year Growth |

17.60% |

|

Companies Covered |

Huawei (China), Ericsson (Sweden), Nokia (Finland), Qualcomm (USA), ZTE (China), Samsung (South Korea), Intel (USA), MediaTek (Taiwan), Cisco (USA), Vodafone (UK), AT&T (USA), T-Mobile (USA), Verizon (USA), LG Uplus (South Korea), China Mobile (China) |

|

Customization Scope |

15% Free Customization (For EG) |

|

Delivery Format |

PDF and Excel through Email |

Carrier Aggregation - Table of Contents

Chapter 1: Market Preface

Chapter 2: Strategic Overview

Chapter 3: Global Carrier Aggregation Market Business Environment & Changing Dynamics

Chapter 4: Global Carrier Aggregation Industry Factors Assessment

Chapter 5: Carrier Aggregation : Competition Benchmarking & Performance Evaluation

Chapter 6: Global Carrier Aggregation Market: Company Profiles

Chapter 7: Global Carrier Aggregation by Type & Application (2020-2033)

Chapter 8: North America Carrier Aggregation Market Breakdown by Country, Type & Application

Chapter 9: Europe Carrier Aggregation Market Breakdown by Country, Type & Application

Chapter 10: Asia Pacific Carrier Aggregation Market Breakdown by Country, Type & Application

Chapter 11: Latin America Carrier Aggregation Market Breakdown by Country, Type & Application

Chapter 12: Middle East & Africa Carrier Aggregation Market Breakdown by Country, Type & Application

Chapter 13: Research Finding and Conclusion

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.